The rules for reporting scope 3 emissions are becoming tighter. The Greenhouse Gas Protocol is revising its Corporate Value Chain (Scope 3) Standard, which is the global standard used to measure and report value chain emissions.

This work is part of the GHG Protocol’s partnership with the International Organization for Standardization (ISO) to create a more consistent global approach to measuring and reporting emissions. This means the changes may matter for companies that use ISO standards, as well as those that follow the GHG Protocol directly.

Its latest progress update is not a final standard, but it signals a clear shift: scope 3 reporting is moving towards more complete, transparent and evidence-based reporting.

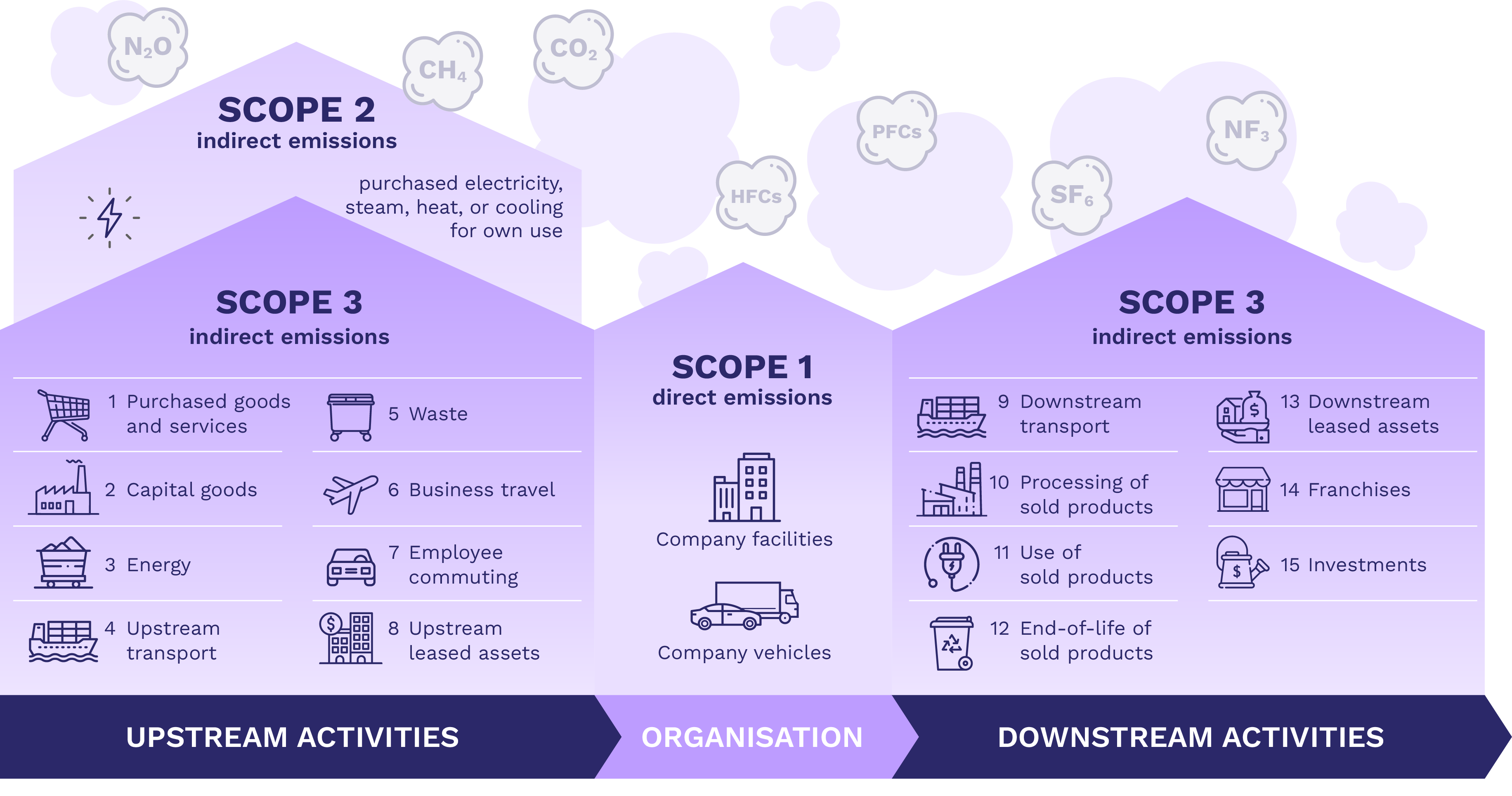

Scope 3 emissions can be tricky to report, as they sit outside a company’s direct operations, across purchased goods, freight, business travel, waste, investments and the use of sold products. They are often the largest part of a company’s carbon footprint and the hardest to measure.

Learn more about the 15 categories of Scope 3

Changes to proposed scope 3 reporting at a glance

- 95% coverage: companies currently need to report scope 3 emissions and explain any exclusions. The proposed change would make this more prescriptive, requiring companies to report at least 95% of their scope 3 emissions.

- 5% exclusions need to be quantified: companies could no longer leave out categories simply because they are hard to measure. They would need to estimate the size of any excluded emissions, show they add up to no more than 5% of their scope 3 emissions, and explain why they were excluded.

- Better data: companies would need to show how they calculated their scope 3 emissions. For example, did the data come directly from a supplier, was it estimated using industry averages or was it calculated from spend data? Companies should also set goals to improve data quality over time, such as increasing the share of emissions based on supplier-specific or primary data. This will make it clearer which parts of the footprint are based on strong evidence and which parts still rely on assumptions.

- Investments in focus: Category 15 covers emissions linked to investments. This may become more relevant not only for banks and investors, but also for non-financial companies with investment portfolios, treasury investments, minority stakes or pension-related exposures. These businesses may need to check whether investment-related emissions should be included in their scope 3 inventory.

- New Category 16: the GHG Protocol is proposing a new category for “other value chain activities”. This could affect businesses that enable or facilitate emissions through their products, services or platforms without owning the activity themselves. Examples may include marketplaces, licensing models, underwriting, insurance-related activities, booking platforms or other fee-based business models. Most of this reporting is still proposed to be optional, but companies with these models should monitor the changes.

When will changes to scope 3 reporting apply?

The current plan is to take the draft revised scope 3 standard to public consultation in the second half of 2026, with the final revised standard expected in late 2027. The timeline may change as the standard goes through consultation and possible pilot testing.

Don’t wait until it is published to get ready. Australian and New Zealand companies that sell into global supply chains may feel the change earlier through customer requests, especially from customers covered by overseas regimes such as the EU’s Corporate Sustainability Reporting Directive.

Why does scope 3 reporting matter for businesses in Australia and New Zealand?

In Australia, large companies are being phased into mandatory climate reporting under AASB S2. In New Zealand, climate-related disclosures already apply to climate reporting entities such as large listed issuers, banks, insurers and investment managers.

Scope 3 reporting matters because it is part of climate disclosures and supply chain emissions often make up most of a company’s carbon footprint. They also rely on data from outside the business, which means customers, suppliers, lenders and investors all become part of the reporting chain and will need to get ready for the new standard themselves.

For businesses, this shows up in practical ways:

- Customer requests: large customers may ask suppliers for emissions data to complete their own climate reports.

- Tender requirements: credible scope 3 data may help suppliers stand out in procurement and contract renewals.

- Finance and insurance: banks, investors and insurers may ask for better emissions data to assess climate risk.

- Supply-chain management: businesses may need to identify high-emissions products, materials, freight routes or suppliers.

- Assurance readiness: companies will need clearer records of data sources, assumptions and exclusions.

Even if a business is not directly covered by mandatory climate reporting, it may still be affected through the value chain. The message is simple: better scope 3 data can help businesses meet reporting expectations, respond to customers and stay competitive.

How to prepare now

- Check coverage: compare your current inventory with the proposed 95% benchmark

- Find the hotspots: identify the suppliers, products, services and investments that drive the largest emissions

- Estimate excluded emissions: work out ways to estimate emissions for any categories you currently leave out, so you can show they make up no more than 5% of your total scope 3 emissions

- Improve supplier data: use shared templates and clear definitions.

- Update contracts: include rights to request emissions data.

- Track data quality: record whether data is primary, supplier-specific, estimated or spend-based.

- Review investments and business models: check exposure to category 15 and proposed category 16.

- Prepare for assurance: keep records of methods, assumptions, exclusions and sources.

The takeaway

Scope 3 reporting is becoming more rigorous. Estimates will still have a role, but businesses will need clearer boundaries, stronger evidence and better supplier data.

The companies that start now will be better prepared for assurance, regulation and customer expectations.